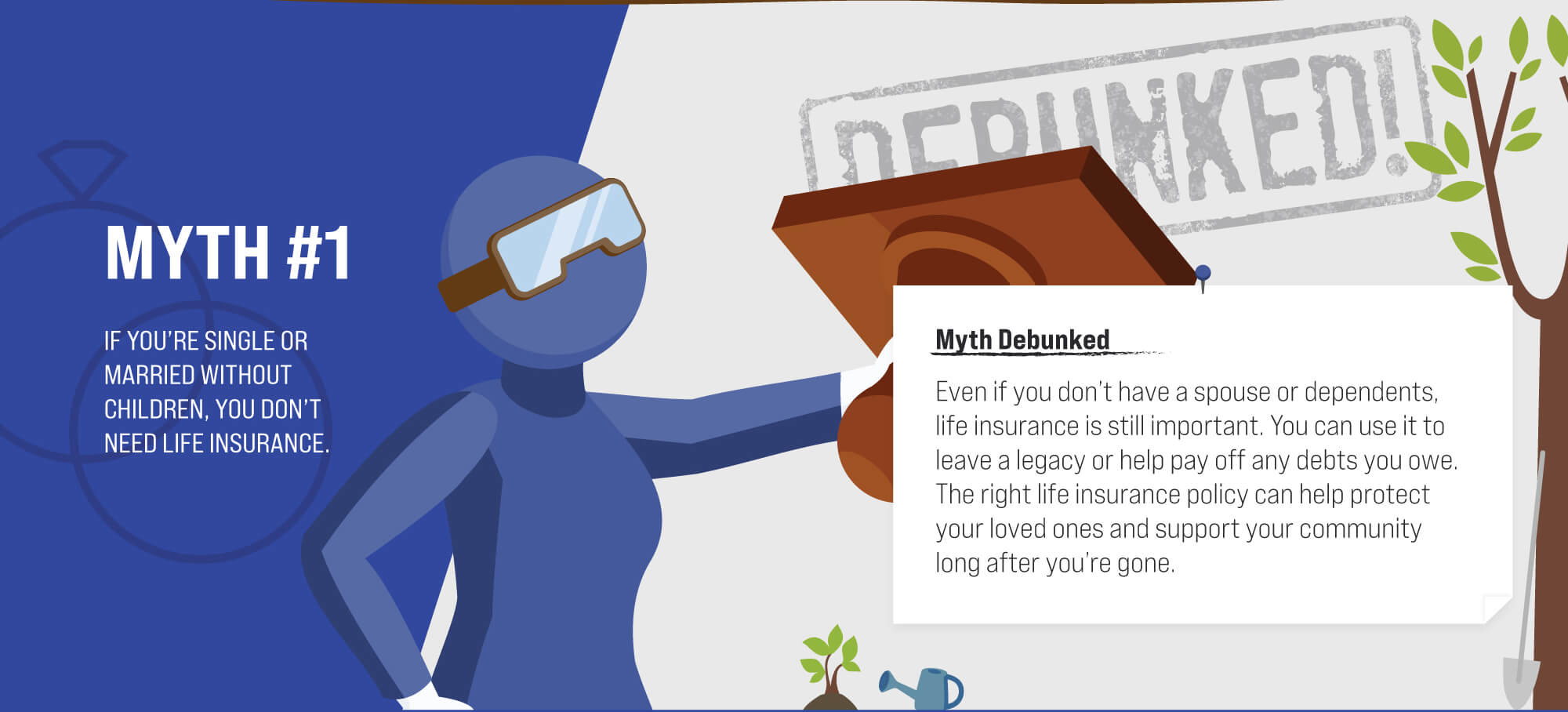

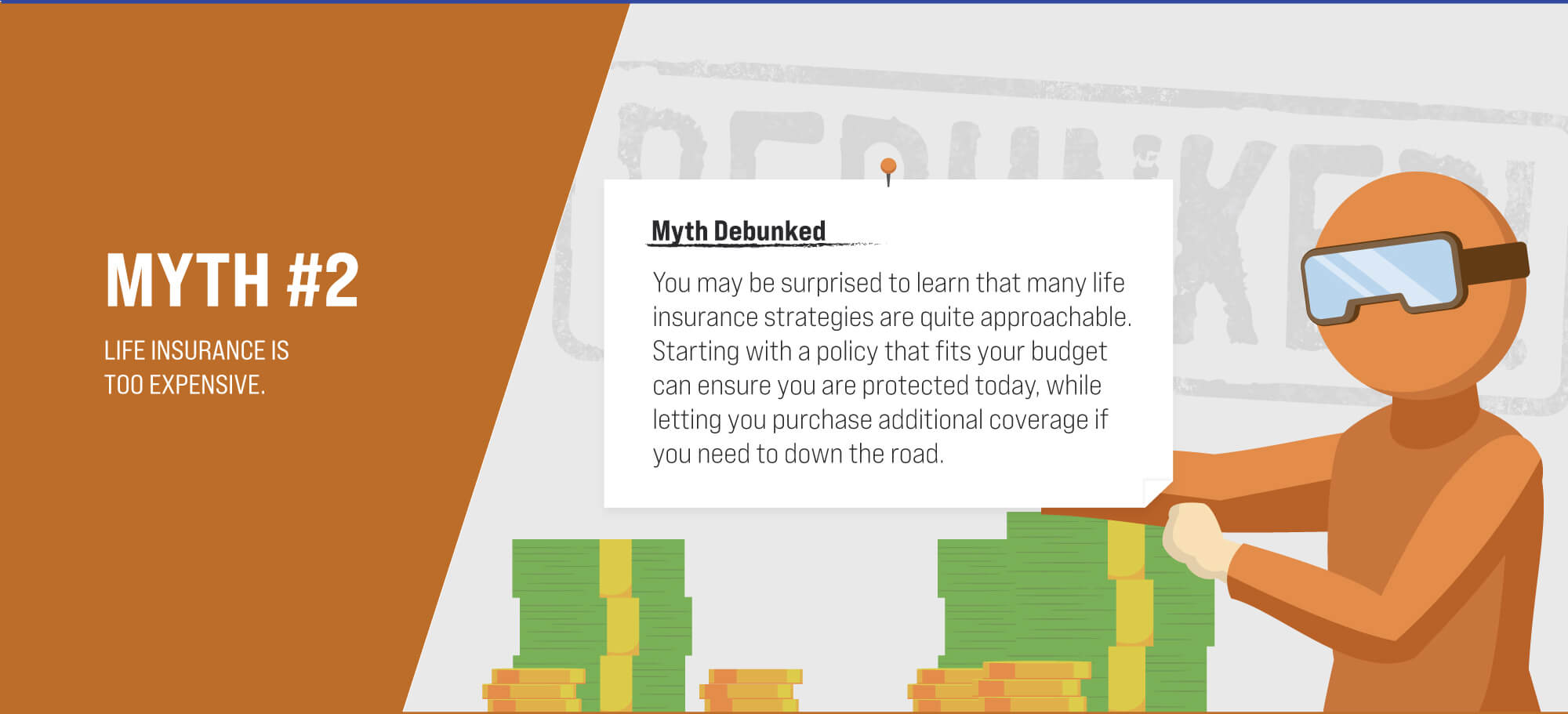

Life Insurance Myths: Debunked

Your liability for damages that occur when a tree on your property falls on your neighbor’s property is not clear cut.

This calculator compares employee contributions to a Roth 401(k) and a traditional 401(k).

The tax rules governing profits you realize from the sale of your home have changed in recent years.